Personal income tax

When looking at the changes to personal income tax in isolation (i.e. ignoring the increase in the VAT rate and the usual increases in “sin taxes”), the budget speech was probably as good as could have been expected.

The most widely predicted changes in some quarters was that there would be an increase in the maximum marginal tax rate as well as the scrapping of the medical tax credit. Fortunately, neither of those have occurred. What has happened, however, is that the full effects of inflation have not been taken into account in making adjustments to the personal income tax rates or the medical tax credit. It is predicted that this will result in additional collections of R6.8 billion.

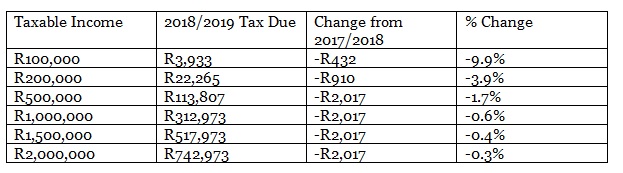

In regard to the personal income tax rates, no adjustments have been made to the top four income tax brackets and below inflation adjustments have been made to the bottom three income tax brackets. In addition, the medical tax credit has been increased from R303 to R310 per month for the first two beneficiaries and from R204 to R209 per month for the remaining beneficiaries. The primary, secondary and tertiary rebates have also been adjusted, with the result that the tax threshold for taxpayers under 65 years of age increases from R75,750 to R78,150.

The effect of the changes to the personal income tax rates will have the following effect at the various taxable income levels for taxpayers under 65:

In addition to the above, there has also been an announcement that the estate duty rate will increase from 20% to 25% for estates in excess of R30 million as well as an increase in the donations tax rate to 25% for donations in excess of R30 million in one tax year. Both of these increases will be effective from 1 March 2018.

From an employer’s perspective, it has been announced that there will be slight increases in the tax free subsistence allowances that can be paid to employees as well as in the tax-free reimbursive travel claim that can be paid to employees for business travel. It is also proposed that the official rate of interest applicable to soft loans to employees by employers will be amended to bring it closer to the prime rate rather than the current repo rate plus 1%. This latter change could have a negative impact on employees in receipt of soft loans from their employer since the rate at which fringe benefits will be determined could increase. On the positive side, however, it seems that for loans provided by employers to employees solely for housing purposes, relief from fringe benefits tax in respect of loans of less than R450,000 will also be provided.

Barry Knoetze is the Associate Director at PwC Tax.

Corporate tax

Amendments to debt relief rules: Taxpayers recently noted that the new debt relief rules introduced during 2017 result in adverse income tax implications. For example, where a taxpayer raises additional share capital and applies the funding so obtained to settle debt, such settlement of debt could result in an increased tax bill if the debt so settled is not with a South African tax resident group company. This is specifically the case where a South African taxpayer wishes to settle debt with an offshore holding company or treasury company. In such a case, the taxpayer would be required to obtain external/third party funding to settle the debt if it does not want to fall foul of the current debt relief rules. In addition, any amendment to the terms of certain loans may also trigger adverse tax consequences.

The Minister of Finance announced that the Government noted concerns about unintended consequences that may arise from the current debt relief rules and it is proposed that further amendments be made to address these concerns. Although it is uncertain which concerns the Minister referred to, a review of the debt relief rules would be welcomed by business as the legitimate restructure of debt may presently result in adverse income tax consequences which may impede business growth.

Alwina Brand is the Partner at PwC Tax.

Tax rules affecting short-term insurers: The much anticipated new Insurance Act (2017) permits foreign re-insurers to conduct reinsurance business in South Africa through a branch of an offshore company. A number of offshore insurance companies are considering opening up operations in South Africa under this new rule.

However, the income tax treatment of such branches appeared to be a draw back as the Income Tax Act provisions regulating the taxation of short-term insurance apply only to short-term insurers resident in South Africa and not to foreign short-term insurers operating through a branch. This would result in an uneven playing field as South African insurers are allowed certain tax allowances in respect of technical insurance reserves which would not be available to the foreign insurers.

It has nevertheless been announced that the income tax provisions applying to South African resident short-term insurance companies will be extended to apply to non-residents operating short-term insurance business through branches in South Africa. This announcement will create clarity with regard to the tax position of foreign reinsurers wishing to operate through branches in South Africa.

It is not clear though whether the announcement in this regard would also extend to controlled foreign companies (so-called CFCs) of a South African resident who operate as licensed short-term insurers in their country of tax residency. At present, the legislation with regard to the income tax treatment of licensed short-term CFCs seem to have the unintended consequence of excluding these entities from claiming allowances in respect of technical insurance reserves.

Alwina Brand is the Tax Partner at PwC.

Abuse of collateral lending arrangements: Legislation is to be introduced to curb schemes where dividends are paid out as manufactured dividends to avoid dividends withholding taxes by foreign shareholders.

Jabu Masondo is the Tax Partner at PwC.

Clarity expected to bad debt allowances: An amendment to the doubtful debts allowance under section 11(j) of the Income Tax Act was made in 2015, with the intention that the allowance would be claimed according to criteria set out in a public notice issued by the Commissioner. The criteria has nevertheless not been formulated and it is now proposed that the criteria for determining the allowance should instead be included in the Income Tax Act. A specific amendment to the Income Tax Act would result in more clarity to business and will be good news.

Alwina Brand is the Tax Partner at PwC.

Boost for electronic communication providers: At present companies that provide telecommunications infrastructure are allowed to write off lines or cables used for the transmission of electronic communications over a period of 15 years under section 11D of the Income Tax Act.

These entities will certainly welcome the announcement that the Government proposes reducing the period over which electronic communication lines and fibre optic cables are written off, in a bid to align the tax system with technological advances and international practice.

A more beneficial tax allowance system would hopefully boost additional investment in fibre optic infrastructure which in turn would stimulate business growth.

Alwina Brand is the Tax Partner at PwC.

Tax treatment of collective investment schemes: It is proposed that the tax treatment of amounts realised by portfolios of collective investment schemes as a result of the trade in underlying assets may no longer purely be taxed as gains of a capital nature. National Treasury notes that some collective investment schemes are trading frequently and arguing, contrary to current case law, that the profits are of a capital nature. Investors are currently benefiting from this tax treatment as the overall return in respect of the collective investment scheme would be enhanced due to the lower effective tax rate.

A move by National Treasury to tax regular trades in collective investment schemes as gains or a revenue nature, would therefore increase the overall tax bill of the collective investment scheme.

Alwina Brand is the Tax Partner at PwC.

International Tax

South Africa has specific anti-tax avoidance legislation aimed at South African owned foreign companies. This so-called controlled foreign company tax legislation in essence aim to tax the notional taxable income of a foreign company in the hands of its South African shareholders. However an exemption is provided from such taxation if the foreign entity is regarded as sufficiently taxed abroad – the threshold is currently set at 75% of the tax that would have been due had the foreign company been a South African tax resident. The rationale for this exemption is that if the foreign company is sufficiently taxed abroad, no or little anti-tax avoidance risk should exist.

In light of the global trend of lowering corporate tax rates, the Minister of Finance proposed that the current 75% “high tax” exemption threshold will be reconsidered. This proposal implicitly recognise that legitimate business may be conducted offshore whilst incurring significantly less foreign tax compared with South Africa. Although a lowering of the 75% threshold would be in line with the global trend, equally important is the manner in which the amount of taxes to be compared are calculated. South Africa’s current “high tax” exemption is not consistent with the global norm (as advocated by the Organisation for Economic Cooperation and development (“OECD”)) and a simple threshold adjustment alone will have little practical impact in respect of foreign companies operating as part of a tax group.

A threshold adjustment (lowering) may still result in the South African shareholders of a foreign company being subject to tax on the notional taxable income of the foreign companies, even though economically the foreign company is subjected to foreign taxes at an effective rate in excess of the “high tax” threshold.

Cor Kraamwinkel is the International Tax Partner at PwC.